If you work in corporate strategy, finance or sustainability, you will have heard about "nature-related risks." In most risk frameworks, embedded in this concept are three very different categories of risk - transition risks, physical risks, and systemic risks. Assessing them properly requires different methods, different data, and different management responses. Confusing them can lead to genuinely bad decisions.

In this article, we map out the history and difference of these three risk categories, in particularly applied to the topic of nature risk assessments. If you want to learn how to properly measure and account for them, scroll down to the end!

Before diving into the categorization, let’s take a step back and try to to unpack the contextual underpinning of these three notions of risk.

The concept of risk is knowingly borrowed from the financial and insurance world, and has been adopted by sustainability practitioners to internalize climate change and environmental collapse into our economic, financial and corporate models. The notions of physical and transition risks, in relation to climate change, were used for the first time on 29 September 2015 by Mark Carney, then Governor of the Bank of England and Chairman of the Financial Stability Board, who gave a dinner address at Lloyd's of London titled Breaking the Tragedy of the Horizon.

During the address, Carney talked about three types of climate change-related risks: physical risk, liability risk, and transition risk. The speech was deliberately aimed at the insurance and finance world, not at scientists or policy theorists.

Carney warned that "a wholesale reassessment of prospects, especially if it were to occur suddenly, could potentially destabilise markets, spark a pro-cyclical crystallisation of losses and a persistent tightening of financial conditions", framing the transition itself as a financial stability risk, and no longer as a simple physical risk. That speech directly led to the creation of the TCFD. The Financial Stability Board, which Carney chaired, set up the Task Force within months. When the TCFD published its 2017 report, it formally codified the two main categories: physical risks as "risks related to the physical impacts of climate change" and transition risks as "risks related to the transition to a lower-carbon economy." It’s worth noting that “systemic risk” was not mentioned in Carney’s speech. As a formal concept, systemic risk has a different and older lineage entirely. It was the 2008 financial crisis that forced this concept onto regulators. In this context, systemic risk was defined as "a risk of disruption to financial services that is caused by an impairment of all or parts of the financial system and has the potential to have serious negative consequences for the real economy."

When applied to other domains, such as climate change or biodiversity loss, systemic risk (as distinct from the risk facing any individual firm) can be seen as a way to capture aggregate risk that is much higher than the simple sum of the individual, localized risks. In other words, systemic risks are about cascading, generalized risks stemming from local risks.

Physical risk is the most straightforward. It refers to the direct, location-specific impact of nature's degradation on your operations or supply chains. Physical risks divide into two sub-categories:

1. Acute (a flood, a wildfire, a pest outbreak)

2. Chronic (gradual soil degradation, declining water quality, long-run pollinator decline).

Both are principally assessed at the level of a specific site or geography. A concrete example: A European coffee roaster sources from a region of the Ethiopian highlands. The forests that regulate rainfall in that region have declined by 40% over two decades. This has increased drought frequency, lowered yields, and raised the roaster's input costs.

Transition Risk

Transition risk refers to the financial exposure created by the policy, regulatory, market, and reputational changes that accompany society's shift toward a nature-positive (or lower-carbon) economy. In other words, it’s not about the direct consequences of nature loss, but it’s rather meant to capture what the response to nature loss leads to.

Transition risks for nature can include (but are not limited to):

Concrete example: A palm oil trader operating in Indonesia has significant operations in areas that will be subject to the EU Deforestation Regulation. If the trader cannot demonstrate legal and deforestation-free sourcing by the time enforcement scales up, the European market (roughly 15% of its revenue) is at risk. That revenue loss is a transition risk.

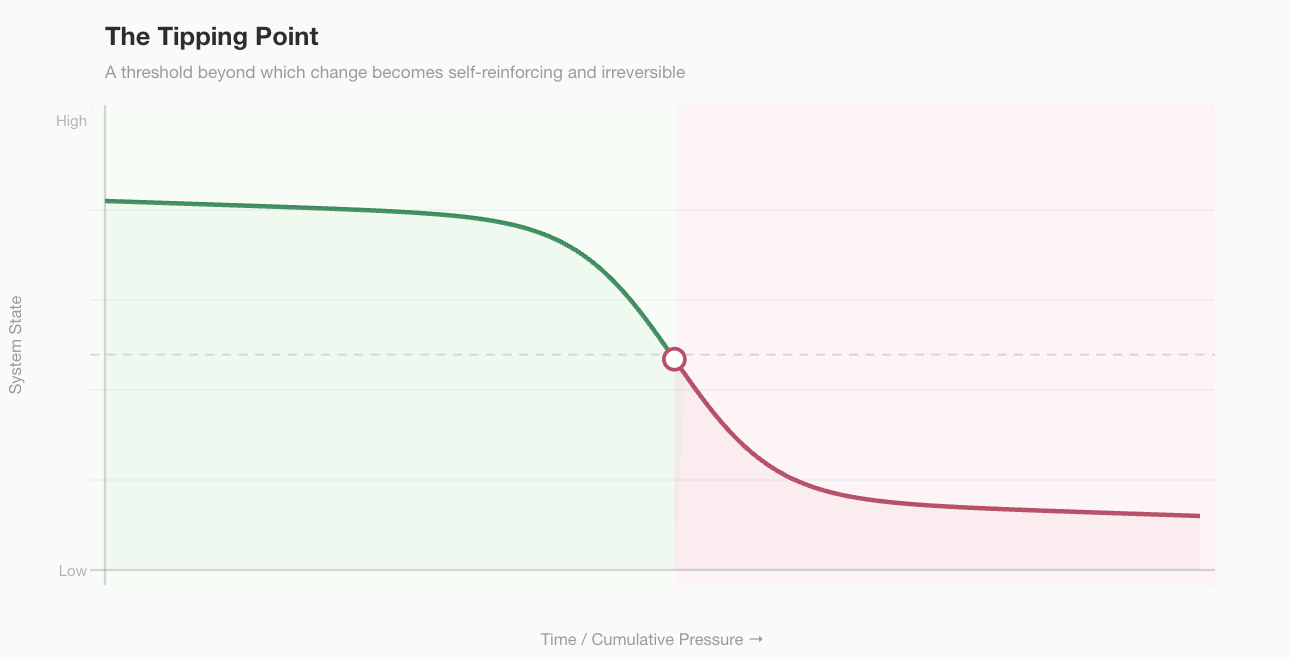

As we have already seen, the notion of systemic risk is definitely the most complex and nuanced of the three. Broadly speaking, it refers to risks that arise from the breakdown of underlying ecological systems so fundamental that they destabilise entire economies, political orders, or social structures - not just individual businesses or assets. The defining feature of systemic risk is that it cannot be diversified away. You cannot hedge against the Amazon rainforest crossing a tipping point, because that event would not harm one sector or one geography: it would alter global rainfall patterns, disrupt agricultural yields across three or four continents, trigger mass migration, and generate geopolitical competition for remaining productive land. All of this would cascade through financial markets simultaneously.

Concrete example: The Amazon is estimated to be approaching a critical threshold (some researchers put this at roughly 20–25% deforestation) beyond which the forest can no longer generate its own rainfall through evapotranspiration and begins to convert to savanna (source: WWF). If that happens, some global commodity markets could face supply shocks of a kind no insurance product, no financial hedge, and no individual company strategy could absorb in isolation. Other systemic consequences could include mass displacement and migrations due to food scarcity, leading to geopolitical instability and conflicts.

A very good description of nature-related systemic risks in action can be found in the UK Government's January 2026 national security assessment, which dives into the linkage between national security and worldwide natural loss.

In common usage, people sometimes describe systemic ecological risks (e.g. the collapse of a critical ecosystem, mass species extinction, the failure of global food systems) as "transition risks" on the grounds that they will force companies and economies to "transition." This framing collapses an important distinction.

Transition risks stem from the managed response to ecological or climate breakdown. It assumes that governments, regulators, and markets will act, and asks: what will that action cost businesses? On the other hand, systemic risks stem from the failure of the underlying natural system. They do not assume managed responses, although they can affect people, societies and markets. In other words: a managed transition that happens well reduces systemic risk. A disorderly transition (e.g. too slow, too late, or badly calibrated) increases systemic risk. But they remain analytically distinct:

The confusion is also partly driven by framework design. Both TCFD and TNFD are built around the concept of double materiality: how risks affect a company, and how a company affects nature. This is a useful lens for governance, but it is inherently firm-centric. Systemic risks, by definition, cannot be adequately captured by aggregating firm-level assessments. The whole is worse than the sum of the parts.

The unpredictability of systemic risk has specific structural causes. These are just some of them:

This fundamentally means that small shocks can produce disproportionately large outcomes.

Ecosystems can absorb pressure for decades while appearing relatively stable, then cross a threshold, also called a “tipping point” in environmental science, beyond which they shift rapidly and irreversibly into a different state. This non-linearity means that extrapolating from current trends is often inconclusive.

Cascading effects aggravate this problem. As the previously mentioned UK Government's January 2026 national security report makes clear, risks from ecosystem degradation cascade through a web of connections that are difficult to trace in advance - both geographically, temporally or scale-wise. Deforestation in one region affects rainfall in another. Rainfall disruption affects crop yields. Crop failures affect commodity prices. Commodity price spikes affect political stability. Political instability affects trade routes.

The IMF has described these as "catastrophic nature-climate outcomes or 'endgames' - such as regional systems failure that cascade to other regions - [which] are plausible scenarios that are very hard to quantify, and therefore dangerously unexplored" (IMF Staff Climate Notes, 2024). If you are interested in learning more about nature tipping points, we highly recommend that you have a look at globaltippingpoint.org.

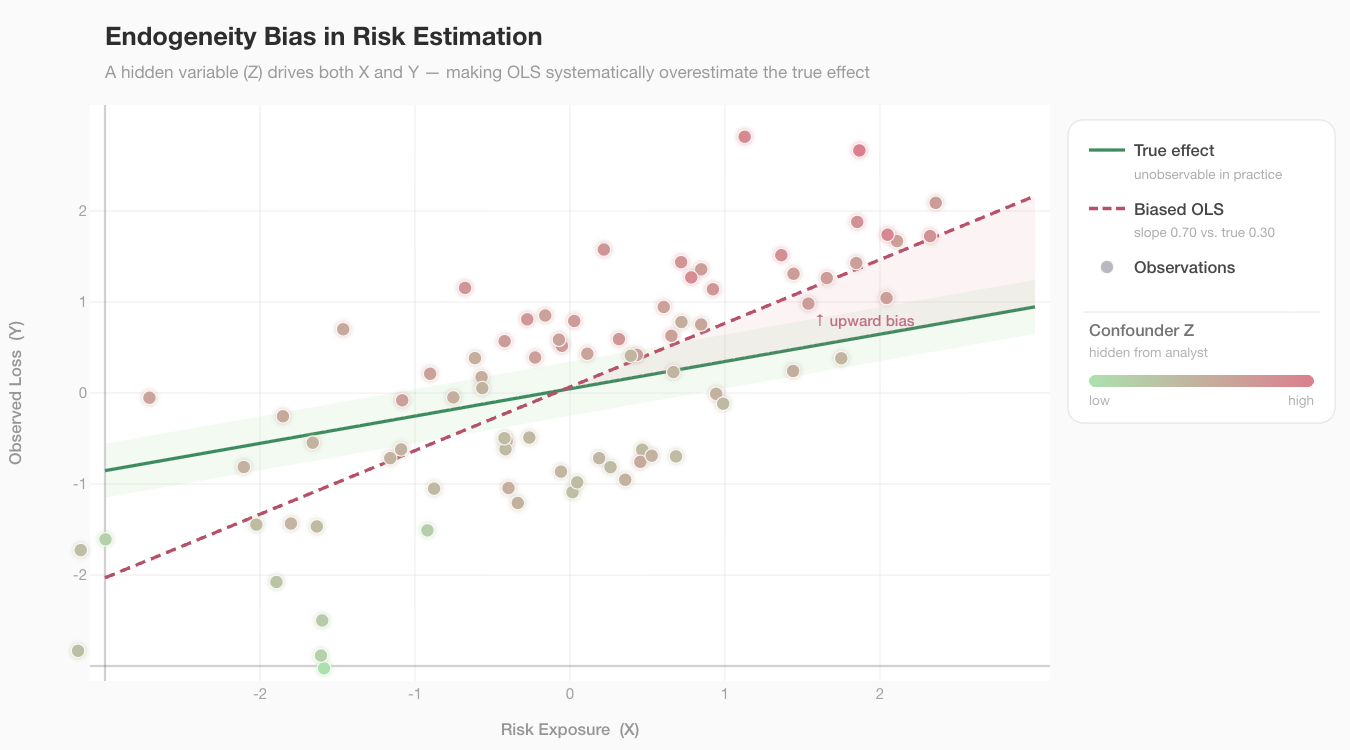

Risks are not always independent of the actions and decisions of the actors exposed to them: a phenomenon known as endogeneity. In the context of nature-related risks, this creates a fundamental modeling challenge: the responses of companies, investors, and governments can collectively shape the very risks they are trying to assess. Endogeneity is especially consequential for systemic risks, such as the cascading effects of ecosystem collapse on supply chains, financial markets, and economies.

Consider a situation where many firms simultaneously depend on the same ecosystem service (e.g. pollination or freshwater provision, for example) and respond to degradation signals in similar ways:

Traditional, static assessment tools treat nature-related risks as external, fixed variables and cannot capture dynamics like these.

Endogeneity is also closely linked to the concept of double materiality: nature risk is often partly produced by the very actors exposed to it. For example:

How this compares to financial endogeneity

This dynamic has a parallel in mainstream finance, where endogeneity appears most visibly in market risk and asset pricing. For instance, large trades move prices, and correlated strategies, like portfolio insurance in the 1987 crash, can create the very downturns they were designed to protect against. The 2008 crisis is often also referred to as at least partially caused by underestimated endogeneity - largely caused by banks and rating agencies, who were responsible for evaluating the risk of those real estate assets, which then exacerbated the risk itself. However, albeit imperfect, financial analysts have developed tools to deal with this. Nature-related risks additionally present a harder version of the same problem: The feedback loops between economic activity and ecosystem degradation are slower, more complex, and less well-documented than those in financial systems, and the data infrastructure is also far less mature.

Unlike many types of financial risks, some of the worst systemic ecological outcomes cannot be reversed by policy intervention.

The classic example: Species extinction. Once a species goes extinct, it cannot be brought back to life (save miraculous technological or scientific advancements). Once a soil or ecosystem has lost its microbiological structure and crossed a tipping point, regeneration takes decades or centuries. This irreversibility means that standard financial models - which tend to assume mean reversion and the eventual recovery of markets - can be poorly suited to the problem.

Uncertainty about timing

Ecosystems are complex adaptive systems with enormous numbers of interacting variables, and small changes in any one of these can propagate unpredictably through the system. This means that even when scientists can identify that an ecosystem is under stress, pinpointing when it will cross a critical threshold is extraordinarily difficult.

Many ecosystems exhibit what ecologists call "slow variable" dynamics, where degradation accumulates gradually and invisibly beneath the surface before manifesting suddenly. Moreover, the triggers for collapse are often external natural shocks (an unusually severe drought, a disease outbreak, a heatwave) whose timing is inherently stochastic and cannot be predicted with precision. The ecosystem may be primed for collapse for years, but the actual event depends on when the right (or wrong) shock arrives. Finally, human behaviour adds another layer of unpredictability: policy decisions, land use changes, and economic pressures can accelerate or temporarily delay degradation in ways that are themselves difficult to forecast.

For all of these reasons, the UK Government's nature security assessment explicitly assigned low confidence to any prediction about the precise timing of ecosystem tipping points, while maintaining high confidence in the direction and systemic nature of the risk. This is the correct epistemic position, but it is uncomfortable for risk models that require probability distributions with specific time horizons.

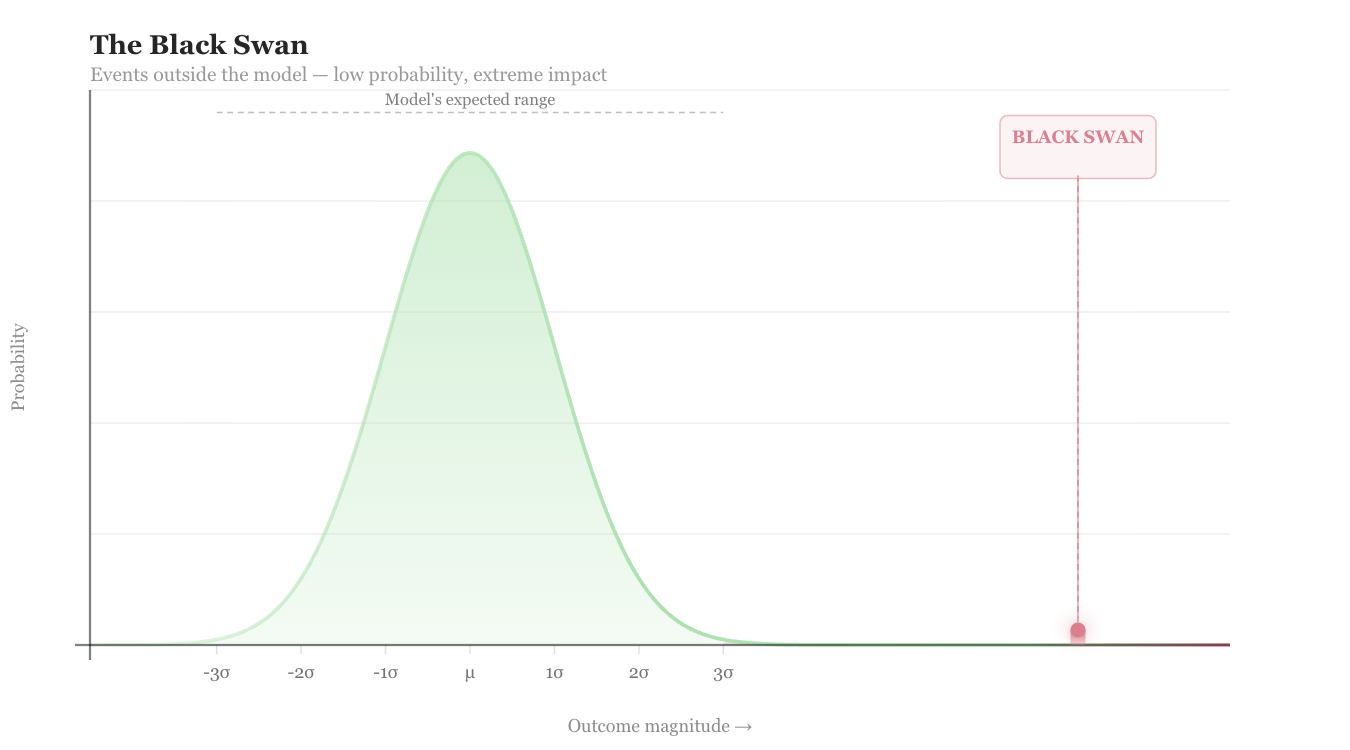

Tail events and black swans

A tail event is a statistical concept referring to any outcome that falls in the "tails" of a probability distribution - meaning it's far from the mean and has a low probability of occurring.

A related but distinct concept is that of black swan event - popularized by Nassim Nicholas Taleb, the idea of black swan refers to an event which is prospectively unpredictable - basically, it lies outside of the model, or unknown unknowns.

While we can often rely on historic data that can be leverage to produce accurate forecasts, many nature-related events (such as abrupt ecosystem collapse, mass species die-offs, or the crossing of planetary tipping points) are often unprecedented in the modern record, meaning there is little or no reliable data from which to estimate their likelihood or severity. This makes conventional statistical tools, which tend to assume risks follow a normal distribution and cluster around an average, dangerously inadequate - they systematically underweight the very events that matter most.

To summarize, nature risk assessments are not trivial. Frameworks like TNFD and ISO 14097 rightly ask organisations to assess the magnitude and likelihood of nature-related risks, but they offer remarkably little practical guidance on how to do this, particularly for systemic risks.

Where does that leave businesses that want to incorporate nature risk assessments into their business risk framework? This does not mean they are powerless, but it does mean they need to approach this topic from a place of high awareness.

Some actionable steps include (but are not limited to):

Above all, the most important step is to understand and communicate the limitations of any assessment methodology you use. No framework (however well-designed) can fully capture the complex dynamics of systemic nature risk, and pretending otherwise creates a false sense of security that is itself a source of risk.

Transition, physical, and systemic risks are not the same thing, do not respond to the same management tools, and cannot be assessed using the same methods. Physical risks are location-specific and can in principle be measured and hedged. Transition risks are policy-dependent, quantifiable through scenario analysis, and require firm-level assessment against plausible regulatory pathways. Systemic risks are non-linear, potentially irreversible, and currently beyond the reach of any individual organisation to fully model or manage, though they must be acknowledged and planned for.

The practical implication is that businesses should carry out an honest assessment about which category of risk they are actually managing. Good transition risk management (that is, starting from the right metrics, the right scenarios, and the right firm-level granularity) is genuinely achievable.

Systemic risk management is much more complex, and requires: collaboration across sectors, engagement with governments and regulators, and support for the ecosystem protection and restoration that is, as the UK Government's report notes, "easier, cheaper and more reliable than relying on yet-to-scale technological solutions."

Key sources: Khan et al. (2024), Nature Climate Change; Fliegel (2025), Corporate Social Responsibility and Environmental Management; IMF Staff Climate Notes (2024); HM Government, National Security Assessment on Global Biodiversity Loss, Ecosystem Collapse and National Security (January 2026); TNFD Final Recommendations (2023); NGFS Scenarios v5.0 (2024).

About prismo

Many corporate sustainability teams struggle to get a scientifically grounded and location-precise understanding of nature-related risks exposures across their assets, and often rely on untestable assumptions or vague frameworks. At prismo, we leverage science, geospatial data and AI to help you with that. You can start today by booking a free consultation with our nature risk experts.

Prismo uses AI to combine high-resolution geospatial datasets, scientific knowledge and company data to produce nature risk insights and compliant nature reports (e.g. TNFD, CSRD) which are grounded in science, but also intuitive and easy to access.

We think that nature risk assessments and reporting should be better, more granular and grounded in real science. This is why prismo is built on deep knowledge and expertise.

Prismo is designed for sustainability teams, investors and procurement teams who want to add nature intelligence to their operations.

The Prismo Earth platform will launch soon. Sign up for our Beta waitlist to access exclusive benefits and get access before others.

We'd love to learn more about the challenges you are facing, and see if we can a be a fit. Please get in touch with us at info@prismo.earth.